“2022 was the year European aviation weathered the storm, with the year closing on 9.3 million flights: 3.1 million more than last year, even if still 1.8 million fewer than 2019”. This is how Eurocontrol’s Analysis for 2022 starts. Nevertheless, Eurocontrol forecasts a good, or better 2023 for European aviation, predicting that in the year to come, traffic will continue to recover.

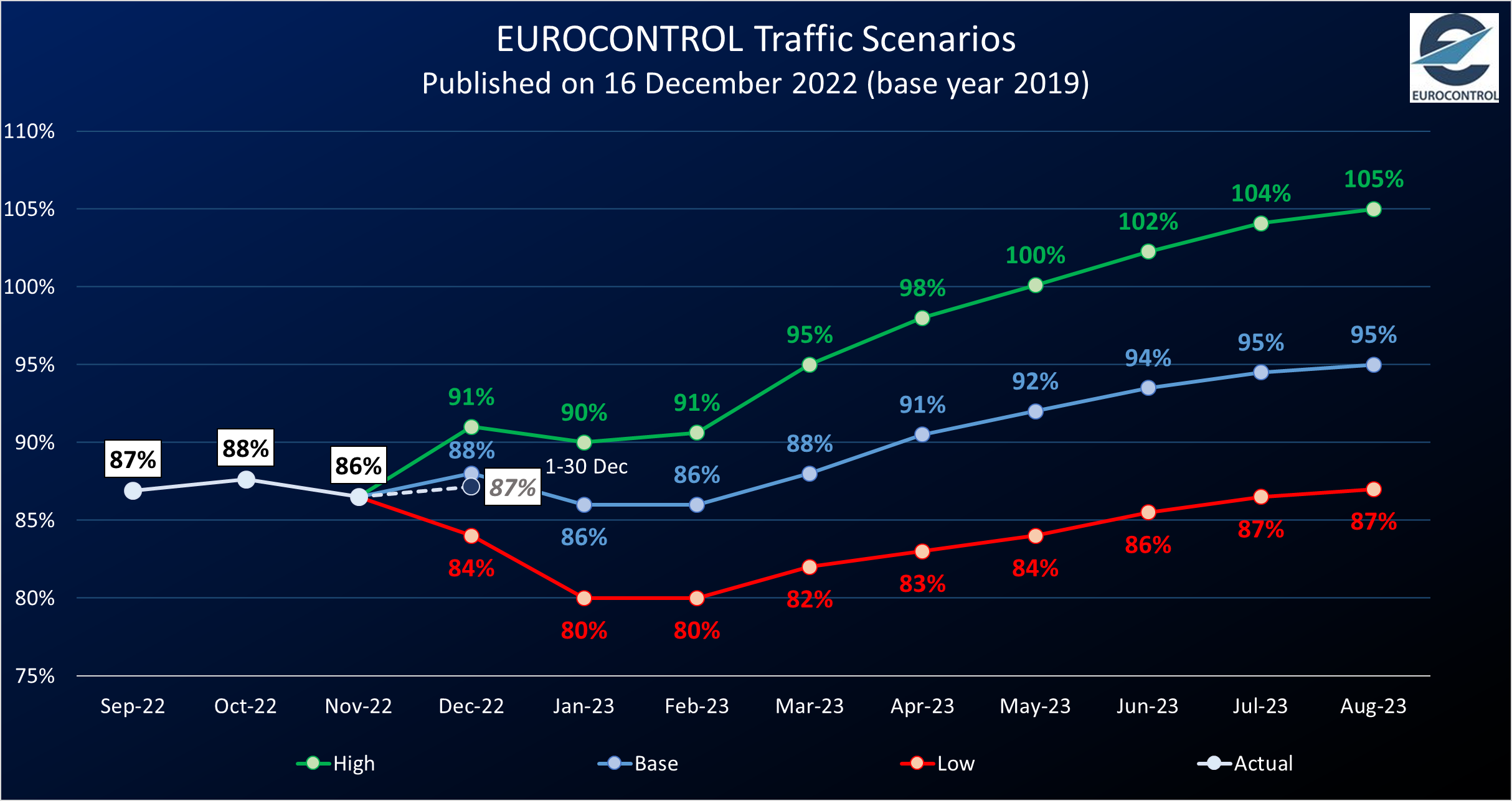

Eurocontrol explains that 9.3 million flights for 2022, represents a solid 83% of 2019 traffic, achieved despite the Omicron spike at the start of the year, and the invasion of Ukraine on 24 February, which continues to have huge socioeconomic impacts on all aspects of the European economy including aviation. In spite of these twin shocks, however, traffic steadily recovered to 86% of 2019 by May, with similar monthly traffic levels ever since.

Eurocontrol’s Analysis Paper digs into the big numbers to track that recovery across the whole of 2022 for every aspect of European aviation, revealing that beneath the global numbers, there is wide traffic variation across airlines, airports, ANSPs and States. Leading the airline recovery in 2022 were the low-cost carriers, overall 85% of 2019 with two top performers in Ryanair (109% of 2019) and Wizz Air (114%); while Europe’s top airports mostly struggled to recover more than 83% of 2019 traffic, Istanbul iGA led the way in first place and around 100% of 2019 levels for most of the year; and at the State level, some of Europe’s smaller or classic holiday destination countries proved the most resilient in recovering to close to or even beyond pre-pandemic levels.

Eurocontrol’s Analysis writes; “As we move into 2023 and beyond, we are confident that the recovery will continue to strengthen as capacity and staffing issues are progressively tackled, even if at a slightly slower pace than we had expected before Russia’s war of aggression. We expect 2023 total traffic will reach 92% of pre-COVID levels, with full recovery from the pandemic to take place in 2025.

But getting closer to pre-pandemic traffic levels will not be easy against a backdrop of supply chain issues, possible industrial action, airspace unavailability, sector bottlenecks, rising demand and system changes. All of this means that 2023 is set to a hugely challenging year for the network, and will require formidable efforts by the EUROCONTROL Network Manager and all operational actors to meet capacity crunches and keep delays down.

For Eamonn Brennan, EUROCONTROL Director General, “the numbers have turned in aviation’s favour. Predictions of pent-up demand were correct and people have shown their desire to take to the skies again as the pandemic has come under control, with summer peaks of 90% or more. There’s still considerable volatility and the recovery is uneven across sectors, but airlines and airports were able in 2022 to rebuild their balance sheets and continue to invest.

Looking ahead, 2023 will pose the biggest challenge in terms of coping with capacity issues and keeping delays down that the network has faced in over a decade. Delays and punctuality need to improve across the network as we get closer to full traffic levels, and connectivity with Europe and especially to the Far East is still considerably lagging pre-pandemic levels. And plans to make aviation sustainable must accelerate if we are to meet our ambitious sustainability targets.

Nevertheless, and despite the ongoing tragedy in Ukraine, our sector has proven its resilience and we are optimistic about the future, with European air traffic set to recover fully by 2025”.

{kind=link}

{kind=link}

{kind=link}